Calculate cost of capital or WACC from equity, debt, preferred stock values, component costs, weights, and tax rate, or solve a missing rate.

- Cost of Debt Calculator

- WACC Calculator (Weighted Average Cost of Capital)

- All Business Calculators

- Cost of Funds Calculator

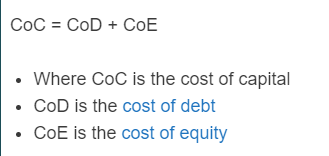

Cost of Capital Formula

In corporate finance, a common way to estimate a firm’s cost of capital is the weighted average cost of capital (WACC):

\mathrm{WACC}=\frac{E}{V}R_e+\frac{D}{V}R_d(1-T_c)+\frac{P}{V}R_p- Where E, D, and P are the market values of equity, debt, and preferred stock

- V = E + D + P is total firm value (total capital)

- Re is the cost of equity (required return on equity)

- Rd is the pre-tax cost of debt (interest rate / yield), adjusted to after-tax by (1 − Tc)

- Tc is the corporate tax rate

- Rp is the cost of preferred stock (if applicable)

Unlike a simple sum of rates, WACC correctly weights each financing source by its share of total capital and adjusts the cost of debt for taxes.

Cost of Capital Definition

What is a cost of capital? The cost of capital is the required rate of return a company must earn on an investment to compensate providers of capital (debt and equity) for the risk they take. It is usually expressed as a percentage per year and is often used as a discount rate for evaluating projects (NPV/DCF) or as a hurdle rate.

Is the cost of capital the same as WACC? WACC is a common estimate of a firm’s overall cost of capital because it blends the required returns of debt, equity (and sometimes preferred stock) using their market-value weights and the after-tax cost of debt. A specific project’s cost of capital may differ from the firm’s WACC if the project’s risk differs from the firm’s average risk.

Why is cost of capital important? Cost of capital is important because it helps determine whether an investment is expected to create value. If a project’s expected return is below the cost of capital, it may destroy value; if it is above the cost of capital, it may create value.

Cost of Capital Example

A company is financed with 60% equity and 40% debt (based on market values). The cost of equity is 10%, the pre-tax cost of debt is 6%, and the corporate tax rate is 25%.

- Equity weight: E/V = 0.60

- Debt weight: D/V = 0.40

- Re = 10%

- Rd = 6%

- Tc = 25%

WACC = 0.60(10%) + 0.40(6%)(1 − 0.25) = 6.00% + 1.80% = 7.80%.

FAQ

In most practical corporate finance settings, the cost of capital (a required rate of return) is not negative. In rare cases, a specific source of financing (for example, subsidized or incentive-based debt) could have an effectively negative after-subsidy interest cost, but a firm’s overall required return is typically still above 0%.

No. Cost of equity is the required return for equity investors only. Cost of capital usually refers to the blended required return across all capital sources (often estimated as WACC), which combines the costs of equity and debt using their weights (and adjusts debt for taxes).