Calculate cost of sales (COGS) from beginning inventory, purchases, and ending inventory, with gross profit and margin details included.

Cost of Sales Formula

There is no single universal “cost of sales” formula because it depends on the type of business. For a manufacturer, cost of sales (COGS) is normally computed using beginning/ending finished goods inventory and the cost of goods manufactured (COGM).

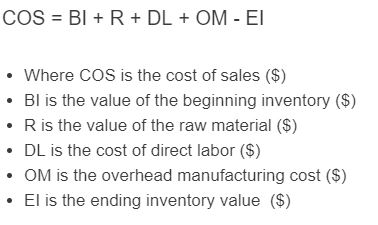

- Where COS is the cost of sales ($)

- BI is the beginning finished goods inventory value ($)

- R is the cost of direct materials used during the period (raw materials put into production) ($)

- DL is the cost of direct labor ($)

- OM is the manufacturing (factory) overhead cost ($)

- EI is the ending finished goods inventory value ($)

Cost of Sales Definition

Cost of sales (often called cost of goods sold, or COGS) is the expense recognized on an income statement for the goods (or services) sold during a period.

Are cost of sales fixed or variable?

Cost of sales usually includes both variable and fixed components. Direct materials and some labor are often variable with volume, while manufacturing overhead can include fixed costs such as factory rent, salaried supervision, and depreciation. As a result, cost of sales often changes with sales volume but is not purely variable.

What factors affect cost of sales?

The following list includes common factors that affect the cost of sales of a product or business.

- The beginning inventory value. This is the total value of your relevant inventory at the beginning of the period (for a manufacturer, often finished goods inventory).

- Ending inventory value. This is the total value of the same type of inventory at the end of the period.

- Direct materials used. This is the cost of materials used to produce goods during the time period (not simply materials purchased).

- Direct labor costs. This is the total cost of labor used to directly produce the product or deliver the service.

- Manufacturing overhead costs. This includes indirect production costs such as indirect labor, factory rent, utilities, maintenance, and depreciation (it excludes selling and administrative expenses).

Why are cost of sales important?

Cost of sales is important because it is used to calculate gross profit and gross margin (gross profit = revenue − cost of sales). Tracking cost of sales over time helps you understand pricing, production efficiency, and inventory impacts. Cost of sales may rise as sales volume rises, but it does not have to move proportionally with revenue due to changes in pricing, product mix, discounts, and cost control.

Can costs of sales be negative?

In normal financial statements, cost of sales is typically not negative. A negative amount can occur in unusual situations (for example, certain accounting adjustments, reversals, or rebates recorded in cost of sales), but it is uncommon. Customer returns are usually recorded through sales returns/allowances (contra-revenue) and inventory adjustments rather than making cost of sales negative in typical reporting.

Cost of Sales Example

How to calculate cost of sales?

- First, determine the beginning finished goods inventory value.

This will be the total value of finished goods inventory at the start of the period being analyzed. For this example, this value is $500.00.

- Next, determine direct materials used.

This is the cost of raw materials put into production during the period (not simply materials purchased). For this example, this is $400.00.

- Next, determine the cost of direct labor.

This is only labor that was directly used to produce the product. For this example, the direct labor is $200.00.

- Next, determine the manufacturing overhead.

Calculate the total manufacturing overhead used. For this example, the overhead is $100.00.

- Next, determine the ending finished goods inventory.

Calculate the total value of finished goods inventory at the end of the period being analyzed. For this example, the ending finished goods inventory value is $200.00.

- Finally, calculate the cost of sales.

Using the simplified manufacturing formula above (assuming no change in work-in-process inventory for the period), COS = 500 + 400 + 200 + 100 - 200 = $1,000.00.

FAQ

Cost of sales (often called cost of goods sold, or COGS) is the expense recognized for the goods or services sold during a period. It generally includes the direct costs of producing or acquiring what was sold and is used to compute gross profit (revenue minus cost of sales).