Calculate capitalized interest for construction projects from accumulated expenditures, rates, and months, or split specific and excess borrowing.

- All Business Calculators

- WACC Calculator (Weighted Average Cost of Capital)

- Cost of Capital Calculator

- Daily Interest Calculator

Capitalized Interest Formula

Capitalized interest is the borrowing cost added to the cost of a qualifying asset, such as a building or construction project, instead of being expensed immediately. The calculator has two modes: a quick estimate and a split calculation for specific borrowing plus excess borrowing.

Quick estimate formula

- CI = capitalized interest

- WAAE = weighted-average accumulated expenditures, or average accumulated expenditures

- r = capitalization interest rate as a percentage

- m = construction period in months

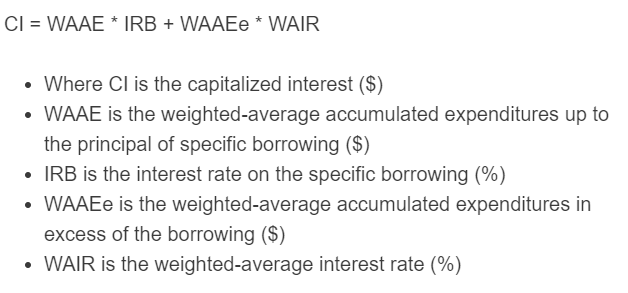

Specific borrowing plus excess borrowing formula

- CI = capitalized interest

- SB = expenditures covered by specific borrowing

- r1 = rate on the specific borrowing as a percentage

- EB = expenditures above the specific borrowing amount

- r2 = weighted-average rate on other debt as a percentage

Use the quick estimate when you have one average expenditure amount, one capitalization rate, and a construction period. Use the specific plus excess borrowing mode when part of the project is financed by a loan taken out specifically for the asset and the remaining expenditures are assumed to be financed by other debt.

Capitalization Rate and Input Reference

| Input | What it represents | Common notes |

|---|---|---|

| Average accumulated expenditures | The weighted average amount spent on the asset during the capitalization period. | Often lower than total project cost if spending occurs gradually. |

| Capitalization interest rate | The interest rate applied to qualifying expenditures. | Use the specific borrowing rate first, then the weighted-average rate on other debt if needed. |

| Construction period | The portion of the year during which interest is capitalized. | A 6-month period is entered as 6, which applies 6/12 of annual interest. |

| Excess borrowing | Qualifying expenditures not covered by specific project debt. | Apply the weighted-average rate from other outstanding borrowings. |

Typical Interest Rate Ranges

| Rate range | Typical use | Effect on capitalized interest |

|---|---|---|

| 4% to 5% | Lower-rate secured or lower-risk borrowing | Lower capitalized interest |

| 6% to 7% | Typical commercial borrowing | Moderate capitalized interest |

| 8% to 10%+ | Higher-risk, subordinated, or more expensive debt | Higher capitalized interest |

Examples

Example 1: Quick estimate

You have average accumulated expenditures of $500,000, a capitalization rate of 6%, and a 12-month construction period.

The capitalized interest is $30,000.

Example 2: Specific borrowing plus excess borrowing

You have $300,000 covered by specific borrowing at 5% and $200,000 of excess expenditures financed at a weighted-average rate of 7%.

The specific borrowing portion is $15,000, and the excess borrowing portion is $14,000. The total capitalized interest is $29,000.

FAQ

What is capitalized interest?

Capitalized interest is interest cost that is added to the cost basis of a qualifying asset instead of being recorded as an immediate interest expense. It is commonly used for assets that take time to get ready for use, such as buildings, major equipment, and construction projects.

When should interest capitalization start and stop?

Interest capitalization generally starts when expenditures for the asset have been made, activities needed to prepare the asset are in progress, and interest cost is being incurred. It generally stops when the asset is substantially complete and ready for its intended use.

Why use weighted-average accumulated expenditures?

Weighted-average accumulated expenditures reflect the timing of spending during the construction period. If you spend money gradually, you did not borrow or use funds for the full project cost for the entire period. Using a weighted average gives a more accurate interest capitalization amount than applying the rate to total project cost.