Calculate equivalent annual cost from purchase price, operating cost, salvage value, discount rate, and useful life, or compare two assets.

- All Business Calculators

- Cost Variance Calculator

- Cost Function Calculator

- Fixed Cost Calculator

- Cost of Debt Calculator

EAC Formula

The calculator uses the capital recovery factor to convert a present cost into an equal yearly payment over the asset's life.

For the total cost mode, the present worth of all cash flows is calculated first, then annualized:

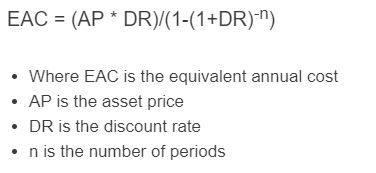

- EAC = equivalent annual cost

- PW = present worth of all costs

- P = purchase price or installed cost

- A = annual operating or maintenance cost

- S = salvage or resale value at end of life

- r = discount rate per year (decimal)

- n = useful life in years

Costs are treated as positive numbers and salvage as a positive recovery. End-of-year cash flow timing is assumed. If you enter a rate of 0%, the formula reduces to PW divided by n. Monthly inputs are converted to annual values before discounting.

Reference Tables

Use the capital recovery factor to sanity-check a result. Multiply your present worth by the factor at your rate and life to get the EAC.

| Life (years) | 3% | 5% | 8% | 10% | 12% |

|---|---|---|---|---|---|

| 3 | 0.3535 | 0.3672 | 0.3880 | 0.4021 | 0.4163 |

| 5 | 0.2184 | 0.2310 | 0.2505 | 0.2638 | 0.2774 |

| 7 | 0.1605 | 0.1728 | 0.1921 | 0.2054 | 0.2191 |

| 10 | 0.1172 | 0.1295 | 0.1490 | 0.1627 | 0.1770 |

| 15 | 0.0838 | 0.0963 | 0.1168 | 0.1315 | 0.1468 |

| 20 | 0.0672 | 0.0802 | 0.1019 | 0.1175 | 0.1339 |

| 25 | 0.0574 | 0.0710 | 0.0937 | 0.1102 | 0.1275 |

Typical discount rates used in EAC analysis depend on the decision context.

| Context | Common rate range |

|---|---|

| Personal purchase, low-risk | 3% to 6% |

| Public sector or utility project | 3% to 7% |

| Corporate capital project (WACC) | 7% to 12% |

| Higher-risk equipment decision | 12% to 18% |

Worked Example

A machine costs $20,000, has $1,500 in annual maintenance, a $3,000 salvage value after 8 years, and the discount rate is 8%.

- Discount factor at year 8: 1 / (1.08)^8 = 0.5403

- PVAF = (1 - 0.5403) / 0.08 = 5.7466

- PW = 20,000 + 1,500 × 5.7466 - 3,000 × 0.5403 = $26,999

- CRF at 8%, 8 years = 0.1740

- EAC = 26,999 × 0.1740 = $4,698 per year

FAQ

When should you use EAC instead of NPV? Use EAC when comparing assets with different useful lives. NPV alone favors longer-lived projects unfairly. EAC puts both options on a per-year basis.

Why does a higher discount rate increase EAC? A higher rate raises the cost of tying up capital, so the annualized burden of the upfront purchase grows.

Can EAC be negative? Yes. If salvage value at the chosen rate exceeds the present worth of purchase and operating costs, the EAC turns negative. This is rare and usually points to a low rate or an inflated salvage estimate.

Should operating costs include taxes and inflation? Use real costs with a real discount rate, or nominal costs with a nominal rate. Mixing them distorts the result.