Calculate effective interest rate, nominal rate, or compounding periods per year from any two inputs with this interest formula calculator.

Effective Interest Rate Formula

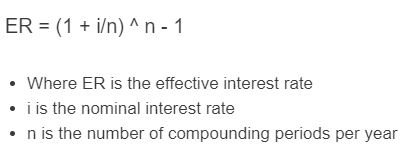

The effective interest rate converts a nominal annual interest rate into the actual annual rate after compounding is included. The calculator uses one formula for regular compounding and another for continuous compounding.

- EIR = effective annual interest rate, in decimal form

- r = nominal annual interest rate, in decimal form

- n = number of compounding periods per year

For continuous compounding, the calculator uses:

- e = Euler’s number, approximately 2.71828

- r = nominal annual interest rate, in decimal form

If you enter a principal amount and a time period, the calculator also estimates the ending balance:

- B = ending balance

- P = starting principal

- EIR = effective annual interest rate, in decimal form

- t = time period in years

The nominal rate field is the stated annual rate before compounding. The compounding frequency field sets the value of n, unless continuous compounding is selected. The optional principal and years fields use the calculated effective annual rate to estimate how much the balance grows over time.

Common Compounding Frequencies

Use this table to see how the selected compounding option maps to the number of compounding periods per year.

| Compounding option | Periods per year | Meaning |

|---|---|---|

| Annually | 1 | Interest compounds once per year |

| Semiannually | 2 | Interest compounds twice per year |

| Quarterly | 4 | Interest compounds every 3 months |

| Monthly | 12 | Interest compounds every month |

| Daily | 365 | Interest compounds every day |

| Continuously | Not fixed | Uses the continuous compounding formula |

Effective Annual Rate Comparison

The more often interest compounds, the higher the effective interest rate becomes for the same nominal rate.

| Nominal annual rate | Compounding | Effective annual rate |

|---|---|---|

| 6.00% | Annually | 6.0000% |

| 6.00% | Quarterly | 6.1364% |

| 6.00% | Monthly | 6.1678% |

| 6.00% | Daily | 6.1831% |

| 6.00% | Continuously | 6.1837% |

Example

Example 1: Monthly compounding

Suppose the nominal annual interest rate is 6%, compounded monthly.

The effective annual interest rate is approximately 6.1678%.

Example 2: Ending balance

Suppose you invest $10,000 for 5 years at a nominal annual rate of 6%, compounded monthly. From the first example, the effective annual rate is about 6.1678%.

The estimated ending balance is about $13,489.35, and the total interest earned is about $3,489.35.

FAQ

What is the difference between nominal interest rate and effective interest rate?

The nominal interest rate is the stated annual rate before adjusting for compounding. The effective interest rate is the actual annual rate after compounding is included. If interest compounds more than once per year, the effective interest rate is usually higher than the nominal rate.

Why does more frequent compounding increase the effective interest rate?

More frequent compounding means interest is added to the balance more often. After each compounding period, future interest is calculated on a slightly larger balance. This creates interest on interest, which raises the effective annual rate.

When should you use continuous compounding?

Use continuous compounding when the interest is modeled as compounding at every instant instead of at fixed periods such as monthly or daily. It is common in finance formulas and theoretical comparisons, but most bank accounts and loans use a stated periodic compounding schedule.