Calculate home affordability by estimating mortgage loan amounts from gross yearly income, term, and APR at 20% to 35% levels for buyers.

Understanding the 28/36 Home Affordability Rule

The 28/36 rule is a simple budgeting guideline for estimating how much house payment may fit your income. The idea is to keep housing costs near 28% of gross monthly income and total required monthly debt payments near 36% of gross monthly income. This calculator focuses on the income, term, and interest-rate side of the decision so you can quickly estimate an affordable mortgage amount before drilling into taxes, insurance, HOA fees, mortgage insurance, and your other debts.

What this calculator is estimating

The calculator starts with your gross yearly income, converts it into a monthly income figure, applies one of several affordability percentages, and then converts that monthly payment budget into an estimated mortgage principal using standard amortization math.

| Income Share | How to Read It | Typical Use |

|---|---|---|

| 20% | Lower monthly payment target with more room for savings and unexpected costs | Conservative planning |

| 25% | Balanced range for buyers who want a moderate payment burden | Middle-ground estimate |

| 28% | Classic front-end affordability benchmark | Common home affordability starting point |

| 35% | Upper-end budget that may feel tight if taxes, insurance, or other debts are high | Stretch scenario |

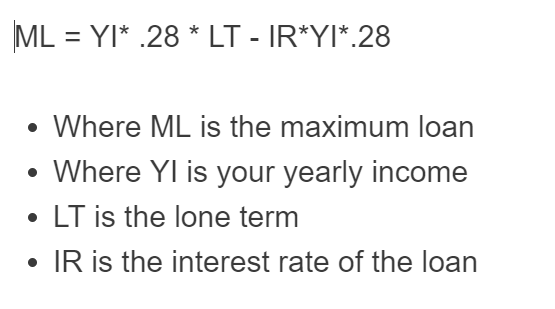

Core formulas behind the calculator

- GMI = gross monthly income

- YI = gross yearly income

- PMT = target monthly housing payment budget

- p = affordability percentage such as 0.20, 0.25, 0.28, or 0.35

- IR = annual mortgage interest rate in percent

- LT = loan term in years

- r = monthly interest rate

- n = total number of monthly payments

- ML = estimated mortgage loan amount, or principal

How the full 28/36 rule should be applied

The calculator gives you a strong payment-based estimate, but the full 28/36 rule has a second step: your housing payment also needs to fit alongside your other required monthly debts. If you already make car, student loan, personal loan, or minimum credit card payments, the 36% side of the rule may become the real constraint.

- HB = housing budget allowed by the full rule

- D = total non-housing required monthly debt payments

If your other debts are low, the 28% test usually drives the answer. If your other debts are high, the 36% test may force a lower home budget even when your income looks strong on paper.

What should be included in your housing payment

For real-world affordability, your monthly housing cost is usually more than just principal and interest. A more realistic budget often includes:

- Principal and interest

- Property taxes

- Homeowners insurance

- HOA or condo fees, if applicable

- Private mortgage insurance, if applicable

That means your principal-and-interest budget may need to be lower than the calculator’s raw payment figure if these extra costs are significant.

- PI = amount available for principal and interest

- TAX = monthly property taxes

- INS = monthly homeowners insurance

- HOA = monthly association dues

- PMI = monthly mortgage insurance

Why the estimated mortgage amount can differ from the home price

The calculator returns an estimated loan amount, not necessarily the exact purchase price of the home. Your down payment bridges the gap between the home price and the amount borrowed.

- HP = estimated home price

- DP = down payment

Example: if the calculator estimates a mortgage amount of $400,000 and you plan to put $80,000 down, your rough target home price would be about $480,000 before closing costs.

Example using the 28% guideline

Suppose your gross yearly income is $120,000, your mortgage term is 30 years, and the interest rate is 6.5%.

In this scenario, the 28% guideline points to a monthly housing budget of about $2,800 and an estimated mortgage principal of about $442,990. If taxes, insurance, HOA fees, and mortgage insurance total $600 per month, the amount available for principal and interest drops sharply.

This is why two buyers with the same income can have very different affordable home prices depending on taxes, insurance, HOA dues, and existing debt.

How to use the calculator effectively

- Enter gross yearly income. Use pre-tax income rather than take-home pay.

- Select a realistic mortgage term. A longer term lowers the payment but increases total interest over time.

- Use a realistic interest rate. Even a small rate change can materially change the loan amount.

- Start with the 28% result. Then adjust downward if you have meaningful non-housing debt or high local housing costs.

- Convert loan amount into purchase price. Add your planned down payment and then subtract estimated closing costs from your available cash.

Why interest rate and loan term matter so much

- Lower rates increase affordability because more of each payment goes toward principal.

- Higher rates reduce the mortgage amount supported by the same payment.

- Longer terms usually increase the amount you can borrow for a given payment.

- Shorter terms usually reduce the loan amount but build equity faster and cut total interest paid.

Common reasons your real budget may be lower than the calculator result

- High property taxes in your area

- Expensive homeowners insurance or flood/wind coverage

- HOA or condo fees

- Mortgage insurance due to a smaller down payment

- Car loans, student loans, or other monthly debt obligations

- Variable or seasonal income

- Maintenance, repairs, utilities, and moving costs

Practical ways to improve affordability

- Increase your down payment to reduce the loan amount

- Compare multiple rate scenarios before choosing a target price

- Pay down existing monthly debt to improve the 36% side of the rule

- Shop by total monthly housing cost, not just list price

- Leave room in your budget for repairs, savings, and emergency expenses

Important interpretation note

This calculator is best used as a planning benchmark. It helps translate income into a reasonable mortgage range, but the most accurate affordability decision comes from combining the calculator result with your down payment, monthly debts, taxes, insurance, HOA dues, and cash reserves. In practice, the safest target is often the payment level that still leaves room for maintenance, savings, and everyday life after the keys are in your hand.