Calculate optimal price from marginal cost and demand elasticity, or find price, cost, or gross margin using target margin pricing.

- All Business Calculators

- Marginal Cost Calculator

- Marginal Revenue Calculator

- Target Profit Calculator

- Cost Volume Profit Calculator

Optimal Price Formula

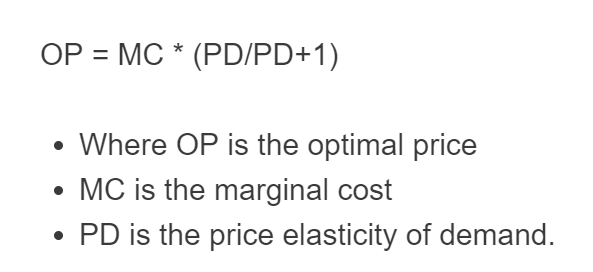

The following markup formula (often associated with the Lerner rule) can be used to estimate a profit-maximizing price when marginal cost is constant and the price elasticity of demand is known.

- Where OP is the optimal (profit-maximizing) price

- MC is the marginal cost per unit

- |Ed| is the absolute value (magnitude) of the price elasticity of demand (it must be greater than 1 for a finite positive solution)

The price elasticity of demand measures how quantity demanded responds to a change in price. To learn more click the link above.

To calculate an optimal price using the formula above, multiply the marginal cost by |Ed|/(|Ed| − 1). (If you use the common convention where Ed is negative, an equivalent form is OP = MC · Ed/(Ed + 1).)

Optimal Price Definition

An optimal price is the price that maximizes total profit under a given set of assumptions about demand and costs. In other words, it is the best balance between price and quantity sold; it is not necessarily the highest price, and it is not necessarily the revenue-maximizing price.

How to calculate optimal price?

How to calculate optimal price?

- First, determine the marginal cost

The marginal cost is the cost of producing one additional unit of product. It can decrease, stay roughly constant, or increase depending on economies of scale and capacity constraints.

- Next, determine the price elasticity of demand

For a more detailed description, visit our PED calculator through the link above. In short, this measures how the quantity demanded changes when the price is changed. You will need to track quantities sold at certain price points to estimate this value.

- Calculate the OP

Calculate the optimal price using the formula above (note that the Lerner-rule formula requires |Ed| > 1 for a finite positive price).

FAQ

An optimal price is the price a good or service should be sold to maximize total profit under a given set of assumptions about demand and costs. This does not necessarily mean maximizing profit per unit. Reducing prices can also lead to more overall profit if more product is sold as a result.

Marginal cost is the cost to produce one additional unit of product. Depending on the production process, marginal cost can decrease, stay roughly constant, or increase as output changes.