Calculate CAPM beta, expected return, levered or unlevered beta, and portfolio beta from returns, risk-free rate, market risk, and weights.

Customize This Calculator

Build your own version. Describe what you want changed, added, or compared.

CAPM Beta Formula

In CAPM, an asset’s expected return is modeled as:

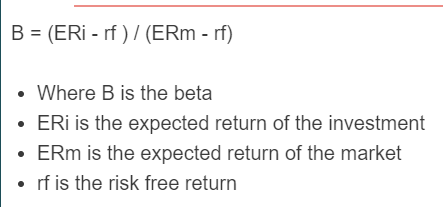

- Where β is the asset’s beta relative to the market (systematic risk / sensitivity to market returns)

- E[Ri] is the asset’s expected return

- E[Rm] is the market’s expected return

- rf is the risk-free rate (often proxied by a short-term government yield in the relevant currency)

If you assume CAPM holds and you already have expected returns, you can rearrange the CAPM equation to get an implied beta:

In practice, beta is most commonly estimated from return data using:

CAPM Beta Definition

In the Capital Asset Pricing Model (CAPM), beta (β) measures an asset’s systematic risk—how sensitive the asset’s returns are to movements in the market portfolio. A beta of 1 means the asset tends to move with the market; greater than 1 means it tends to amplify market moves; less than 1 means it tends to be less sensitive.

Can CAPM Beta be negative?

Yes. Beta can be negative when the asset’s returns tend to move opposite the market on average (i.e., the covariance between the asset and market returns is negative). Negative betas are uncommon for broad equities but can occur for certain assets or strategies that hedge market risk.

What does beta mean in CAPM?

In CAPM, beta is a measure of exposure to market risk, not a measure of whether an investment is “good” or “bad.” If the market risk premium is positive, CAPM implies higher-beta assets should have higher expected returns to compensate for higher systematic risk, but a higher beta does not guarantee better realized performance.

What is zero beta CAPM?

In the standard CAPM (with a risk-free asset), an asset (or portfolio) with β = 0 has an expected return equal to the risk-free rate. In Black’s zero-beta CAPM (a version of CAPM that does not rely on borrowing/lending at a risk-free rate), the intercept is the zero-beta rate, which does not have to equal the risk-free rate.

Is CAPM beta levered or unlevered?

CAPM uses the beta of the asset you are valuing. For publicly traded companies, the beta you typically see quoted is the equity (levered) beta. Analysts often “unlever” equity beta to compare business risk across firms (asset/unlevered beta) and then “relever” it to a target capital structure.

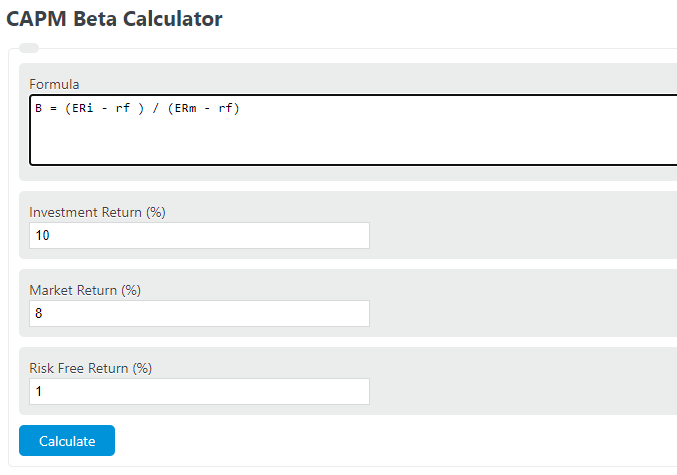

CAPM Beta Example

How to calculate CAPM beta?

- First, determine the return of your investment.

Estimate the expected return of your investment.

- Next, determine the return of the market.

Estimate the return of the market over the same time period.

- Next, determine the return of a risk-free asset.

This is often proxied by short-term government securities (for example, Treasury bills) in the same currency.

- Finally, calculate the beta.

Estimate beta from return data (covariance/variance) or solve for the implied beta by rearranging the CAPM equation, depending on what inputs you have.

FAQ

In CAPM, beta (β) measures an asset’s systematic risk—how sensitive its returns are to movements in the market portfolio. It is commonly estimated as Cov(Ri, Rm) / Var(Rm).