Calculate levered beta from unlevered beta, tax rate, debt, and equity, or solve any missing value with the capital structure formula.

Related Calculators

- Collateral Coverage Ratio Calculator

- Hurdle Rate Calculator

- Lease Discount Rate Calculator

- Risk Premium Calculator

- All Business Calculators

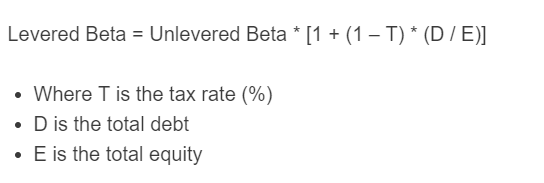

Levered Beta Formula

Levered beta, also called equity beta, measures how sensitive a company’s equity is to overall market movements after considering the effect of debt. It starts with unlevered beta, which reflects business risk without financing choices, and then adjusts that risk for the company’s capital structure.

| Input | Meaning | Practical note |

|---|---|---|

| Unlevered Beta | Business risk before debt is considered | Often estimated from peer companies and then adjusted to a target capital structure |

| Tax Rate | Corporate tax rate used in the leverage adjustment | If entered as a percent, 25% corresponds to 0.25 in the algebra behind the formula |

| Debt | Total interest-bearing debt | Using market value is generally preferred when available |

| Equity | Total shareholder equity or market capitalization | Debt and equity must be expressed in the same units |

| Levered Beta | Equity risk after adjusting for leverage | This is the beta typically used in CAPM-based cost of equity estimates |

How to Use the Levered Beta Calculator

- Enter the unlevered beta, tax rate, debt, and equity if you want to solve directly for levered beta.

- If the calculator allows any three values, provide three known fields and solve for the missing one.

- Use the same currency and same date basis for debt and equity so the ratio is meaningful.

- Check that equity is not zero and that the tax rate is in a realistic range.

Rearranged Forms

If you know levered beta and want to solve for another variable, these equivalent forms are useful.

Unlevered beta from levered beta

Tax rate from the other variables

Debt from the other variables

Equity from the other variables

What the Result Means

- Higher levered beta usually means the stock is more sensitive to market swings.

- More debt relative to equity generally increases levered beta, all else equal.

- Higher tax rates reduce the size of the leverage adjustment because interest tax shields offset part of debt’s impact.

- If a company has no debt, levered beta and unlevered beta are the same.

- A beta above 1 suggests greater market sensitivity; below 1 suggests lower sensitivity.

Example

Suppose a company has an unlevered beta of 0.90, a tax rate of 25%, debt of $300,000, and equity of $600,000.

The levered beta is approximately 1.24. That means the company’s equity risk is meaningfully higher than its underlying business risk because debt amplifies shareholder exposure.

Levered Beta vs. Unlevered Beta

These two measures answer different questions:

- Unlevered beta isolates operating or asset risk.

- Levered beta shows the risk borne by equity investors after financing choices are included.

Analysts often unlever peer betas, average them, and then relever the result to a target debt-to-equity structure.

Why Levered Beta Matters in Valuation

Levered beta is commonly used in the Capital Asset Pricing Model to estimate a company’s cost of equity.

Because cost of equity feeds directly into discount rates, valuation models, hurdle rates, and capital budgeting decisions, using an appropriate levered beta is important whenever capital structure differs across companies.

Common Mistakes to Avoid

- Mixing book value debt with market value equity without considering whether that mismatch is acceptable for the analysis.

- Using debt and equity from different reporting dates.

- Entering the tax rate inconsistently as a whole number in one place and a decimal in another.

- Assuming a higher beta always means a better or worse investment; beta measures sensitivity, not quality.

- Ignoring that negative or extremely high values may signal unusual capital structure or input errors.

FAQ

- What does a levered beta greater than 1 mean?

- It generally means the stock is expected to move more than the market on average, indicating higher systematic risk for equity holders.

- Why does debt increase beta?

- Debt creates fixed financial obligations. When operating results change, those fixed claims can magnify the gains or losses that remain for shareholders.

- Should I use market values or book values?

- Market values are usually preferred for valuation work because beta is a market-based risk measure. Book values may still be used when market values are unavailable.

- Can levered beta be lower than unlevered beta?

- It can happen in edge cases, but under a normal positive debt load and a realistic tax rate, levered beta is usually higher than unlevered beta.

- When is unlevered beta more useful?

- Unlevered beta is especially useful when comparing companies with different capital structures or when estimating a beta for a business that is changing its debt policy.